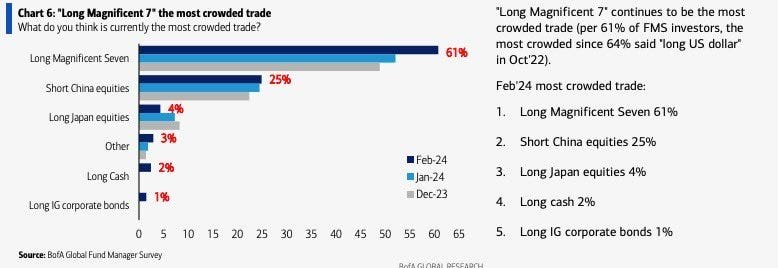

Hiện tại trade được đông đảo các nhà quản lý quỹ thực hiện nhất là “Long Mag-7”, với 61% số người trả lời survey này của BofA. Đây là mức cao nhất kể từ tháng 10 năm 2022 với 64% các nhà quản lý quỹ lúc đó trả lời “Long USD”.

Lịch sử các “crowded trade” của BofA survey.

Điều này cộng thêm với các yếu tố technicals khác như seasonality, positioning, sentiment, inter-market divergence, volatility etc. và các yếu tố macro khác như lạm phát có khả năng tăng trở lại, QRA, FED nghiêng về phía “hawkish” hơn là “dovish”, etc. theo mình sẽ khiến khả năng trái phiếu, thị trường tài sản rủi ro (cụ thể là chứng khoán Mỹ) đứng trước việc điều chỉnh giảm trong thời gian này là lớn hơn việc nó tiếp tục tăng giá.

Phát biểu của Uchida - BoJ.

Nói chung có rất ít những phát biểu của các ngân hàng trung ương mà mình thấy … hay. Đa phần là nhàm chán và chỉ đọc vì đấy là việc phải làm. Tuy nhiên bài phát biểu hôm 8/2 vừa qua của Uchida thì phải nói là hay và làm sáng tỏ rất nhiều góc nhìn thị trường của BoJ.

Speech by Uchida Shinichi

Thường thường anh em sẽ thấy rất nhiều các bài phân tích mà suy nghĩ không thấu đáo về Nhật Bản sẽ có cái kiểu nói chung chung là: À, làm phát tăng rồi, giờ các CBs khác cùng tăng lãi suất, BoJ không thể nào giữ chính sách thế này nữa. Điên rồ! hay là Như thế này thì sẽ huỷ hoại đồng Yen, BoJ không thể để việc này diễn ra được. vân vân vân vân.

Hay là thêm vào được tí carry trade unwind, rồi Nhật Bản là nước có đầu tư ra nước ngoài lớn nhất trên thế giới, flows quay lại Nhật là vô cùng lớn nếu BoJ thay đổi chính sách (bullish Yen), vvv. Nói chung là muốn bắt short JGBs, long Yen vì cái ý tưởng BoJ PHẢI thay đổi chính sách này.

Nhưng bài phát biểu này của Uchida giải thích rõ ràng toàn bộ chiến lược của BoJ một cách rất sâu sắc và cung cấp các lý do vì sao BoJ vẫn tiếp tục theo đuổi chính sách nới lỏng của mình. Tất cả các điểm mà Uchida nói đều có thể mang ra tranh luận được, tuy nhiên mình vẫn là trader đi theo quy tắc “Don’t fight the FED” hơn là ông ổng lên cãi nhau chứng minh tôi đúng ông (CBs) sai.

Một vài điểm cần lưu ý trong bài phát biểu:

Chính sách tiền tệ ở Nhật Bản không phản ứng nhanh như các quốc gia khác do có quá nhiều các yếu tố cấu trúc (structural) đang diễn ra. Họ không thể máy móc tăng lãi suất khi lạm phát tăng lên khi cả quốc gia vẫn đã và đang đối mặt với deflation mindset trong vài thập kỷ qua, nhân khẩu học (demographic) xấu, và một r-star thấp.

Lịch sử Nhật Bản có liên quan và ảnh hưởng tới chính sách tiền tệ đương đại, Nhật Bản không phải Mỹ và Châu âu.

Trong khi rất nhiều CBs quan tâm tới vòng xoáy giá cả và tiền lương, BoJ lại hoan nghênh điều này xảy ra. Tình trạng thiếu hụt lao động và tiền lương cao hơn là cách tốt nhất để BoJ tái cơ cấu nền kinh tế Nhật Bản.

Logic “lạm phát tăng lên, đã tới lúc nâng lãi suất” không áp dụng được với Nhật Bản do bức tranh tổng thể lớn và phức tạp hơn rất nhiều.

Sau đây là một vài charts và trích dẫn của bài phát biểu này:

BoJ dự báo lạm phát tại Nhật Bản sẽ rơi xuống dưới 2% trong 2024-2025

Virtuous Cycle between Wages and Prices

Going forward, the Bank will monitor developments in the virtuous cycle between wages and prices by carefully examining various data and information. On this basis, if sustainable and stable achievement of the 2 percent target comes in sight, the large-scale monetary easing will have fulfilled its role and the Bank will explore whether it should be revised. Given that this large-scale easing has been in place for more than 10 years, regardless of the timing of policy revision, the Bank needs to devise both communication and market operations so as not to create discontinuity in financial markets before and after the revision. From this perspective, it is important for the Bank to explain its basic thinking on potential revisions to individual measures, as far as is possible.

Policy Interest Rate

The Bank's basic thinking is to examine the current situation of and outlook for economic activity and prices, and then set the policy interest rate at an appropriate level so that CPI inflation will be at around the 2 percent target. On this basis, the actual path naturally depends on future economic and price developments. That said, given the outlook I explained earlier, even if the Bank were to terminate the negative interest rate policy, it is hard to imagine a path in which it would then keep raising the interest rate rapidly. The Bank would, I think, maintain accommodative financial conditions even if the termination were to take place.

Business Management in an Economy with Labor Shortages

Here, I believe that we have finally started to come up with a clue to resolving the fundamental issue of strengthening Japan's growth potential. Labor shortages may be distressing to individual firms, but they also bring opportunities. Specifically, labor shortages drive individual firms' transformation and improve the metabolism of the economy from the vantage point of working people, by prompting firms to build profit models that enable sustained wage hikes and to make efforts to attract people to work for them. Of course, since capitalism involves competition, this does not mean that it will benefit all. "Economic metabolism" usually has a positive connotation and, to my mind at least, is often used in a somewhat facile manner, but the hard reality is that it implies the exit of a certain number of firms from the market. Some firms may look back wistfully at the deflationary period, which allowed them to get by as long as they did not overextend themselves. Absent such dynamism, however, we cannot expect Japan's economy as a whole to recover its growth potential amid a declining population. Therefore, I think that a realistic solution will be to proceed with economic metabolism with minimum transition costs. Economic metabolism led by labor shortages entails relatively low transition costs, in that it is less likely to give rise to unemployment. Nevertheless, not everyone who was working may be able to find a new job right away, so this metabolism will still involve pain. In this sense, it is encouraging that, recently, there are an increasing number of cases in which firms pursue mergers and acquisitions as well as business succession because they are attracted to the employees who work for the target firms.

Norm during the Deflationary Period

Meanwhile, in Japan's transition out of deflation, firms' business strategies have been hindered by the social behavior and norm in which people assume that wages and prices will not increase or change. Firms are of the view that, under this deflationary norm, it has been difficult for them to move in the direction of making better products and raising prices. However, it is not necessarily clear through which channels this norm has adversely affected the economy. From a theoretical perspective, it should be possible to change relative prices of individual products regardless of the overall inflation rate. Please look at Chart 14.

One possible argument here is that changing this norm would make it easier for firms to adjust wages. Even now, firms sometimes remark that, since raising base pay would increase fixed costs, they would choose lump-sum payments for wage adjustments. This mindset assumes deflation or zero inflation. In economies in which inflation continues to be at around 2 percent every year -- for example, economies like Europe and the United States, as well as Japan in the 1980s -- even if a firm raises base pay too much in one year, this would not create an increase in its fixed costs because it can make up for this rise by adjusting base pay increases from the following year.

Furthermore, if overall nominal wages increase every year, individual firms would be able to adjust wages more flexibly in line with factors such as their business performance or, for example, to attract younger workers or specialized human resources. This could be an advantage of changing the norm during the deflationary period. However, I am not entirely convinced that this alone would be a game changer for society. While the narrative of the norm during the deflationary period often refers merely to the phenomenon where wages and prices do not increase, I believe that it is necessary to regard this norm as being more complex, involving underlying economic, social, and political structures.

These structures include fierce competition among firms and chronic demand shortages, loose labor market conditions and anxiety about employment, and various safety nets that enabled firms to get by somehow. In particular, a decisive factor, in my view, was "the situation where firms could hire people without having to raise wages." Over the past 10 years, even though Japan's economy is no longer in deflation, it has been so hard to overcome this norm. I think that this is because it took a long time for the remaining scope of increasing labor supply to narrow and for a true "labor shortage economy" to come about.

In this sense, although the trigger has been cost-push factors originating overseas, wages in Japan have in fact been rising, and I feel that the stage is now being set for Japan's economy to change. We are now facing the opportunity to break out of the mindset and behavior of the deflationary period and bring about an economy where wages and prices increase. If firms devise business models that enable this, and people choose to work at firms that succeed in doing so, there would be an opportunity to realize an economy with greater overall growth potential.

The Bank will conduct its monetary policy to maintain stable and accommodative financial conditions and support these changes so that they will take root. "A state with positive interest rates" will not be achieved merely through the Bank raising interest rates. It will only be possible if economic activity and prices improve, thereby realizing the situation where raising interest rates is appropriate.

Theo mình ý nghĩa chính sách nghiêng về phía dovish nhiều hơn.

BoJ đơn giản là họ không vội vàng gì cả. JPY tuy yếu nhưng các công ty ở Nhật Bản đã và đang thay đổi để thích ứng với điều này, lạm phát thì đang giảm, dầu không phải là một vấn đề quá đáng ngại, và Nikkei thì đang lên như rồng như hổ. Thêm vào đó, chúng ta có:

2 quý liên tục GDP Nhật Bản tăng trưởng âm

Cho nên theo mình BoJ vẫn sẽ tiếp tục chính sách nới lỏng của họ trong năm nay.

Tuy nhiên đối với cá nhân mình thấy USDJPY vẫn là US yields trade nhiều hơn là BoJ trade. Và với tình hình USDJPY tiệm cận đỉnh cũ 15x (level mà MoF can thiệp) thì …

MoF và USDJPY level mà họ sẽ can thiệp (Yentervention).

Chúng ta lại vừa được thấy Kanda và Suzuki xuất hiện trên báo chí liên tục tuần vừa qua:

*JAPAN'S SUZUKI: RAPID FX MOVES ARE UNDESIRABLE *JAPAN'S SUZUKI: FX SHOULD MOVE STABLY REFLECTING FUNDAMENTALS *JAPAN'S SUZUKI: WATCHING FOREX WITH STRONG SENSE OF URGENCY *KANDA: IN CLOSE COMMUNICATION WITH BOJ *KANDA: WE DON'T TAKE FX ACTION BASED ON SPECIFIC LEVELS *KANDA: 10-YEN MOVE OVER ONE MONTH IS RAPID *KANDA: ALWAYS READY TO TAKE MEASURES 24 HOURS A DAY, 365 DAYS *JAPAN'S KANDA: SOME OF THE MOVES LOOK SPECULATIVE *KANDA: WILL TAKE APPROPRIATE STEPS ON FX AS NEEDED *KANDA: RAPID FX MOVES HAVE NEGATIVE IMPACT ON ECONOMY *KANDA: WATCHING FOREX WITH HIGH LEVEL OF URGENCY *KANDA: WILL TAKE APPROPRIATE MEASURES ON FOREX *KANDA: RECENT FX MOVES ARE RAPID

Chart của Brent Donnelly

Chúng ta có thể dễ dàng thấy cứ lúc nào Kanda lên báo đài nói chuyện “urgency” nhiều là USDJPY chuẩn bị điều chỉnh. Các lần trước phát biểu của Kanda đều na ná nhau và không thực sự cung cấp được thông tin có giá trị nào ngoài việc giúp anh em ta chuẩn bị tinh thần cho volatility spike trên các cặp xxxJPY. Tuy nhiên lần này Kanda có vẻ như đã lộ bài:

"Recent currency moves are rapid. The yen has weakened by nearly 10 yen over the period of one month or so, such a rapid move is not good for the economy," Kanda, the vice finance minister for international affairs. (Source: Reuters)

Sự can thiệp vào tỉ giá USDJPY của MoF luôn được dựa trên 2 yếu tố là mức giá và tốc độ. Và lần này Kanda nói rằng sự dịch chuyển 10-Yen trong một tháng là nhanh và không tốt cho nền kinh tế.

Okay, chúng ta có một ít dữ liệu để dự đoán level tiếp theo mà MoF sẽ can thiệp.

USDJPY và vạch đỏ là mức giá thấp nhất tháng trước.

Mức giá thấp nhất tháng 1 của USDJPY là 140-141, còn đáy 30-ngày so với hiện tại là khoảng 146. Cộng 10-yen vào khoảng giá này chúng ta có level mà MoF có khả năng can thiệp rơi vào tầm 150-156 (range hơi rộng). Hiện tại thì chưa có dấu hiệu nào cho thấy MoF đã can thiệp cả, nhưng có khả năng USDJPY bulls cảm thấy bất an với 15x level nên khu vực này đang chứng kiến rất nhiều áp lực bán.

Mình thì mình vẫn nghiêng về phía USDJPY tăng tiếp hơn do mình bullish US yields. Tuy nhiên mình đang bet volatility sẽ tăng nên bullish xxxJPY cảm thấy không hợp lý lắm trong giai đoạn này, mình sẽ TP long USDJPY hôm nọ trade US CPI ở đây gọi là có ít lộc xuân.

Giờ chờ đợi xem Short US Stock Indexes của anh em ta có chạy tốt không.

Cheers!

Cảm ơn anh em vì đã đọc Anh Họa Sỹ Trading. Nếu thấy hay hãy chia sẻ cho các trader khác nhé anh em!